LIC Single Premium Endowment (Plan 717) – Calculator

Plan Highlights:

- Plan Name: LIC Single Premium Endowment Plan

- Plan Number: 717

- UIN: 512N283V03

- Launch Date: 01 October 2024

- Withdrawal Date: Not Withdrawn / Currently Available

- Current Status: Active LIC Plan

| Year | Age | Premium Paid | Accrued Bonus | Death Benefit | GSV | Maturity Value |

|---|

LIC Single Premium Endowment Plan 717 Calculator

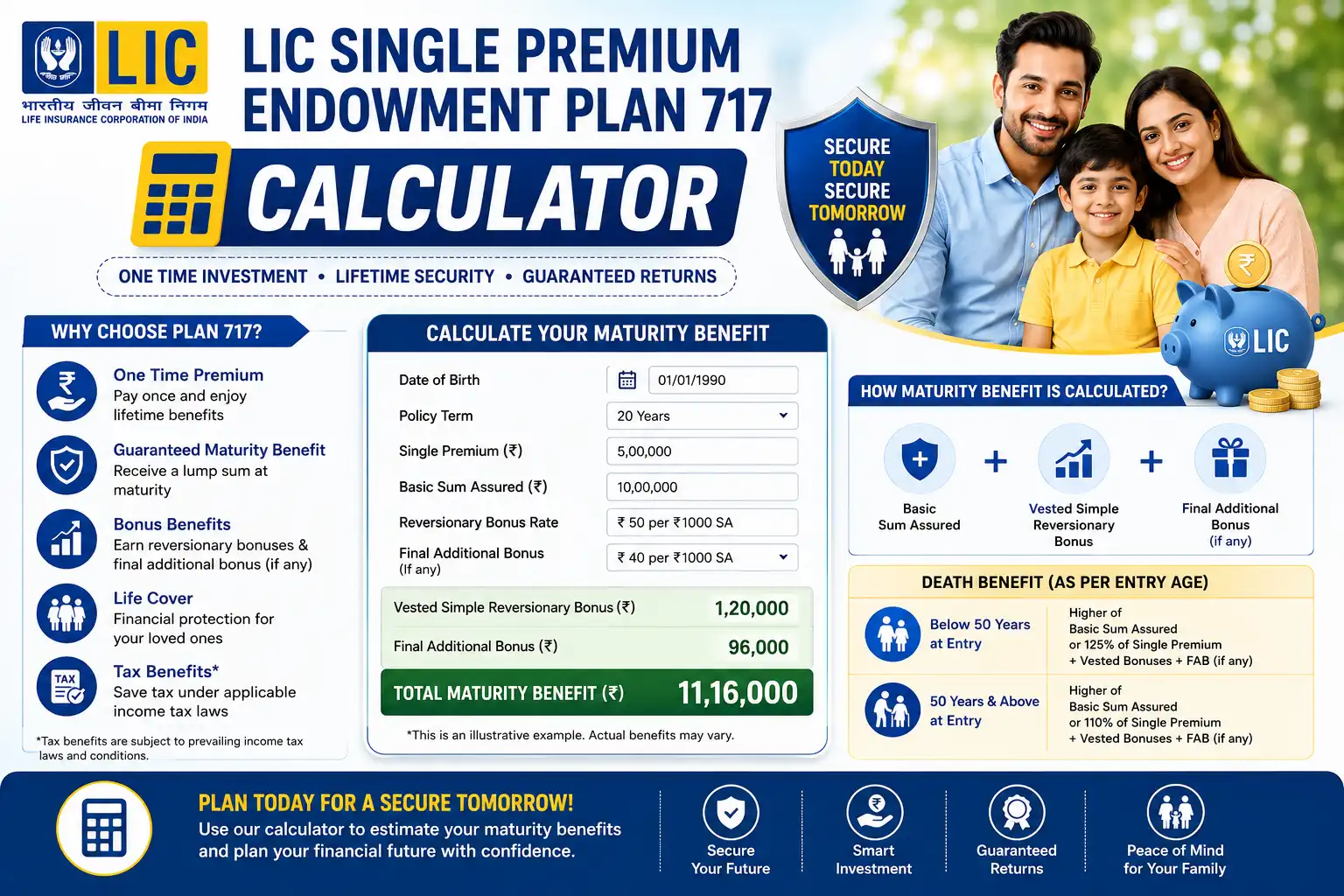

The LIC Single Premium Endowment Plan 717 Calculator helps you estimate maturity value, death benefit, bonus accumulation, and surrender value before investing. Since this policy requires only a one-time premium payment, many investors use the calculator to understand whether the plan fits their long-term financial goals.

Unlike regular endowment plans, you pay the premium only once at the start of the policy. After that, the policy remains active for the selected term while providing life insurance protection and participation in LIC’s profits through bonuses.

LIC Single Premium Endowment Plan 717 Premium & Maturity Calculator

The calculator helps estimate:

- Single premium payable

- Basic Sum Assured

- Maturity benefit

- Death benefit

- Bonus accumulation

- Surrender value

- Overall policy value

Maturity Value Results

The maturity estimate is generally based on:

Basic Sum Assured

+ Vested Simple Reversionary Bonus

+ Final Additional Bonus (if any)

Since future bonuses are declared by LIC from time to time, actual maturity values may differ from projections.

Quick Plan Summary

| Feature | Details |

| Plan Name | LIC Single Premium Endowment Plan |

| Plan Number | 717 |

| Plan ID | UIN: 512N283V03 |

| Plan Type | Participating Endowment Plan |

| Premium Payment | Single Premium |

| Minimum Sum Assured | ₹1,00,000 |

| Maximum Sum Assured | No Limit |

| Policy Term | 10 to 25 Years |

| Bonus Eligibility | Yes |

| Loan Facility | Available |

| Maturity Benefit | Available |

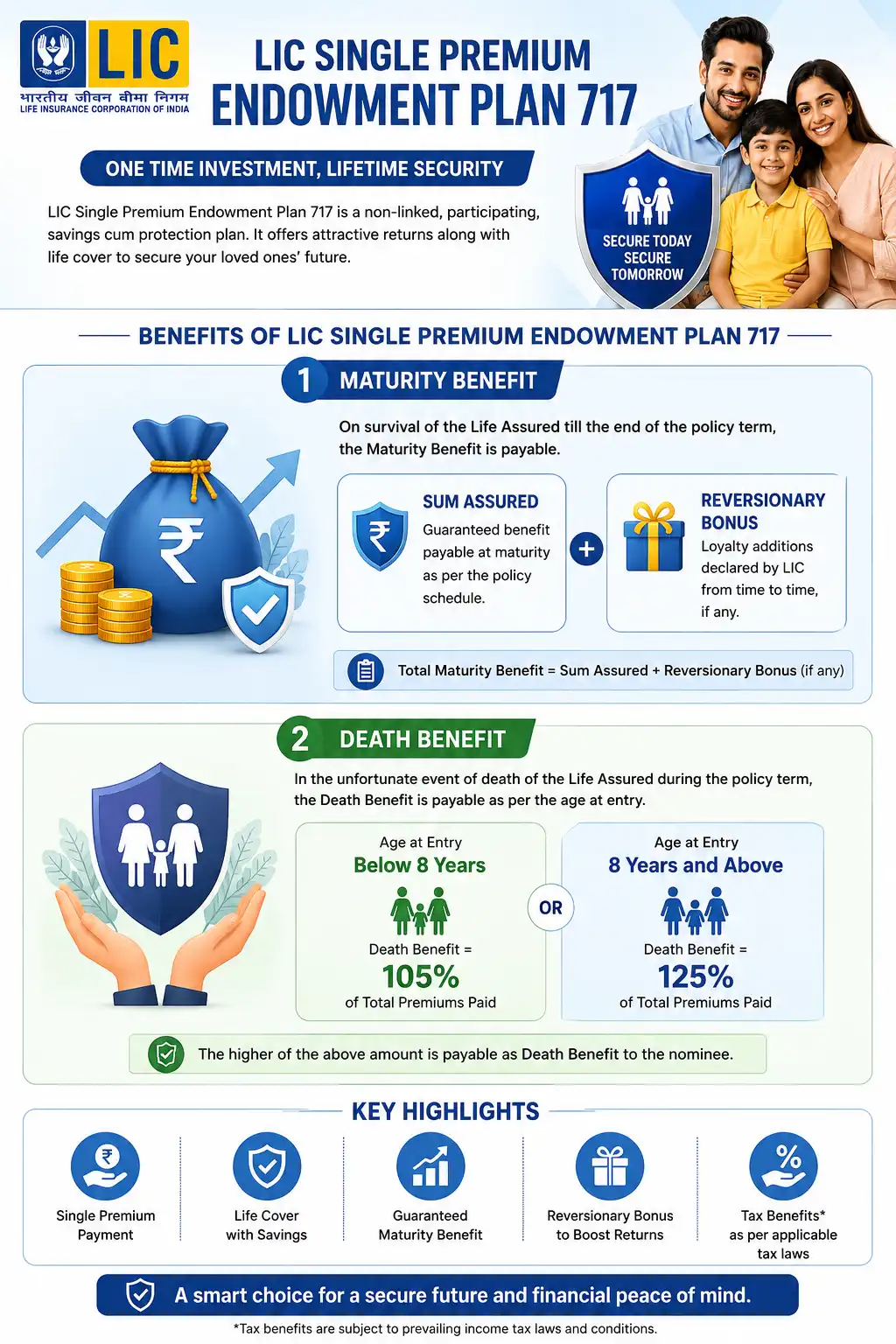

What is LIC Single Premium Endowment Plan 717?

LIC Single Premium Endowment Plan 717 is a participating, non-linked life insurance plan that combines savings and life cover through a single premium payment.

Once the premium is paid, there are no future premium obligations. The policy remains active throughout the chosen policy term while earning eligible bonuses and providing death benefit protection.

This makes it suitable for individuals who have a lump sum amount available and prefer avoiding yearly premium commitments.

Key Features of LIC Single Premium Endowment Plan 717

- One-time premium payment

- Life insurance protection

- Maturity benefit

- Death benefit

- Participation in LIC profits

- Simple Reversionary Bonus

- Final Additional Bonus

- Loan facility

- Guaranteed surrender value provisions

- High Sum Assured rebate

Participating Endowment Plan Overview

A participating plan shares LIC’s profits through bonus declarations.

Eligible policies may receive:

- Simple Reversionary Bonus

- Final Additional Bonus

These bonuses increase the overall value of the policy. However, future bonus rates are not guaranteed and depend on LIC’s declarations.

LIC Single Premium Endowment Plan 717 Eligibility Criteria

Entry Age, Policy Term & Sum Assured

| Criteria | Details |

| Minimum Entry Age | 30 Days |

| Maximum Entry Age | 65 Years |

| Maximum Maturity Age | 75 Years |

| Minimum Basic Sum Assured | ₹1,00,000 |

| Maximum Basic Sum Assured | No Limit |

| Policy Term | 10 to 25 Years |

High Sum Assured Rebate

Higher sum assured levels may qualify for High Sum Assured Rebate, reducing the effective premium rate.

For investors planning larger investments, comparing different sum assured options through the calculator can be useful.

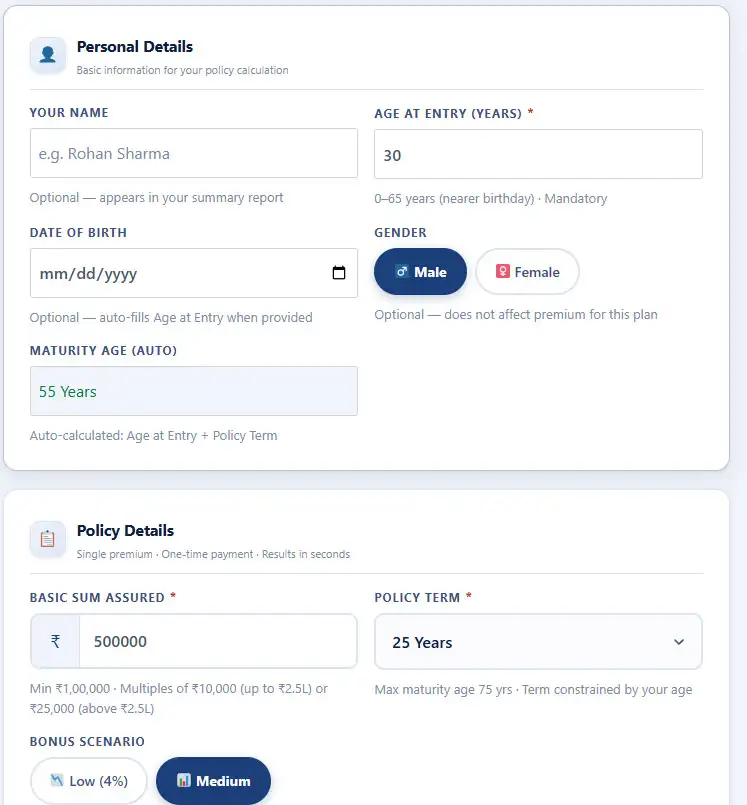

How LIC Single Premium Endowment Plan 717 Calculator Works

The calculator estimates policy benefits based on user inputs.

Required Inputs

Typically, you need:

- Age

- Gender

- Basic Sum Assured

- Policy Term

Premium, Bonus & Maturity Calculation Method

The calculator estimates:

Single Premium

+ Estimated Bonus

+ Estimated Final Additional Bonus

= Estimated Maturity Value

Because bonus declarations change over time, calculator results should be treated as illustrations rather than guarantees.

LIC Single Premium Endowment Plan 717 Maturity Calculator

The maturity calculator helps estimate:

- Maturity amount

- Bonus accumulation

- Total policy value

- Long-term return outlook

Comparing multiple policy terms often gives a better understanding of potential maturity values.

LIC Single Premium Endowment Plan 717 Benefits

Maturity Benefit

If the life assured survives the policy term, the maturity benefit consists of:

Basic Sum Assured

+ Vested Simple Reversionary Bonus

+ Final Additional Bonus (if any)

Death Benefit

According to the brochure:

For age below 50 years at entry

Higher of:

Basic Sum Assured

OR

125% of Single Premium

+ Vested Bonuses

+ Final Additional Bonus (if any)

For age 50 years and above at entry

Higher of:

Basic Sum Assured

OR

110% of Single Premium

+ Vested Bonuses

+ Final Additional Bonus (if any)

Bonus Benefits

Eligible policies participate in LIC’s profits through:

- Simple Reversionary Bonus

- Final Additional Bonus

Over long policy terms, bonus accumulation can become a significant portion of the maturity benefit.

Tax Benefits

Premiums paid and benefits received may qualify for tax benefits under prevailing tax laws, subject to applicable conditions.

LIC Single Premium Endowment Plan 717 Surrender Value Calculator

Sometimes policyholders may need funds before maturity.

The surrender value calculator helps estimate the amount available upon surrender.

Guaranteed Surrender Value

Guaranteed Surrender Value depends on:

- Single premium paid

- Policy duration

- Applicable surrender factors

Special Surrender Value

LIC may also offer Special Surrender Value according to prevailing rules and policy conditions.

Loan Facility

One useful feature of Plan 717 is the availability of a policy loan facility.

Instead of surrendering the policy, eligible policyholders may borrow against it while keeping the policy active.

LIC Plan 717 Benefit Illustration & Sample Calculation

Example:

Age: 35 Years

Policy Term: 20 Years

Basic Sum Assured: ₹10,00,000

Premium Type: Single Premium

The calculator estimates:

- Premium payable

- Maturity value

- Death benefit

- Bonus accumulation

- Surrender value

These estimates help investors compare different policy structures before investing.

LIC Single Premium Endowment Plan 717 Bonus Rates

Bonus rates are declared by LIC and may vary over time.

Because future bonus declarations are uncertain, it is wise to view calculator projections as planning estimates rather than guaranteed outcomes.

Buy this plan primarily for protection, disciplined savings, and long-term stability—not solely for bonus expectations.

LIC 717 Plan Details PDF Download & Brochure Highlights

The official brochure remains the most reliable source for understanding:

- Eligibility conditions

- Benefit structure

- Riders

- Surrender provisions

- Settlement options

- Loan facility rules

Using the brochure alongside the calculator provides the clearest understanding of the plan.

Related LIC Plans You May Also Compare

If you are evaluating Plan 717, you may also find these calculators useful:

- New Endowment Plan 714

- New Jeevan Anand Plan 715

- Jeevan Lakshya Plan 733

- Jeevan Labh Plan 736

- Bima Jyoti Plan 760

- Amritbaal Plan 774

For example, if you prefer regular premium payments instead of a one-time premium, the New Endowment Plan 714 or New Jeevan Anand Plan 715 may be worth comparing.

Similarly, parents planning for a child’s future may also explore Jeevan Lakshya 733 and Amritbaal 774.

Important Things to Consider Before Buying

Before investing, ask yourself:

- Do I have a lump sum amount available today?

- Can this money remain invested for the selected policy term?

- Am I looking for savings plus insurance protection?

- Do I need liquidity in the near future?

A common mistake is investing emergency funds into a long-term insurance policy.

Frequently Asked Questions (FAQs)

What is LIC Single Premium Endowment Plan 717?

It is a participating endowment policy that combines life insurance protection and savings through a one-time premium payment.

What is the maturity benefit under LIC Plan 717?

The maturity benefit includes Basic Sum Assured, vested bonuses, and Final Additional Bonus (if any).

How does the LIC Single Premium Endowment Plan 717 Calculator work?

The calculator estimates maturity value, bonus accumulation, death benefit, surrender value, and policy value using plan parameters.

What is the surrender value of LIC Plan 717?

The surrender value depends on policy duration, premium paid, bonuses, and applicable surrender value factors.

Is a loan facility available under LIC Plan 717?

Yes. Eligible policies may avail a loan facility according to LIC rules.

Can I download the LIC 717 Plan Details PDF?

Yes. The official LIC brochure contains complete plan information and benefit details.

Does LIC Plan 717 provide bonus benefits?

Yes. Eligible policies may receive Simple Reversionary Bonus and Final Additional Bonus.

Final Verdict And My Point Of View

The LIC Single Premium Endowment Plan 717 Calculator is a practical tool for estimating maturity value, bonus accumulation, death benefits, and surrender value before making a one-time investment. It helps investors understand how the policy may perform over different policy terms and sum assured levels.

The plan is best suited for individuals who have a lump sum amount available and want a combination of life insurance protection, savings, and bonus participation without future premium commitments. Before investing, compare multiple policy terms, review brochure provisions carefully, and use the calculator to understand projected benefits. A few minutes of planning today can help you choose a policy structure that supports your long-term financial goals.

LIC’s All Endowment Plan Calculators

LIC Insurance Plans

Mohibul Islam

LIC Agent & Web DeveloperMohibul Islam is an LIC agent with 7+ years of experience. He also works in web development and blogging. He creates simple tools on LIC Plan Calculator to help people understand LIC plans, calculate benefits, and make better financial decisions easily. Read More About »