LIC Surrender Value Calculator Web App – 2026

Calculate Guaranteed Surrender Value (GSV) and estimated Special Surrender Value (SSV) for all LIC traditional plans — Endowment, Money Back, Limited Pay, Single Premium and Whole Life.

| Year | Premiums Paid | GSV % | GSV on Prem | Accrued Bonus | Bonus GSV | Total GSV | Status |

|---|

Are you considering surrendering your LIC policy? Then our LIC Surrender Value Calculator will make your calculation easy. With just a few simple inputs, you can get an accurate estimate of the amount you’ll receive upon surrendering your policy.

This valuable LIC Surrender Value Calculator Web App helps you to make informed decisions about your life insurance investment and financial planning.

It is very important to know before surrender your policy: What surrender value means and how it can impact your financial goals. In this detailed guide, I’ll tell you pros and cons of LIC surrender value, including how to calculate it using our calculator.

So read the entire article to understand the ins and outs of surrendering your LIC policy and make an informed decision.

What is LIC Surrender Value?

Let’s start with the basics.

LIC Surrender Value is the amount you get when you decide to end your LIC policy before its maturity date. Essentially, you’re breaking the contract with LIC and giving up your insurance coverage. But, you don’t walk away empty-handed.

You’re entitled to a portion of the premiums you’ve paid over the years, and that’s what we call the surrender value.

Now, here’s an important point to note. Not all LIC policies allow you to surrender from day one. Most policies have a lock-in period, usually 3 years, during which you can’t surrender your policy. This is to ensure that policyholders stay committed to their life insurance plan for a reasonable time.

How to Calculate Surrender Value of LIC Policy

Calculating the surrender value of your LIC policy involves a few factors. Let’s break them down:

- Policy tenure: The longer you’ve held the policy, the higher the surrender value. In the early years, a big chunk of your premiums goes towards covering admin costs and mortality charges. But as your policy matures, more of your premiums get invested, leading to a higher surrender value.

- Premiums paid: The more premiums you’ve paid, the higher the surrender value. But it’s not a simple straight-line relationship. LIC uses complex actuarial formulas to determine the surrender value, considering the time value of money and the expected future premiums.

- Type of policy: Different LIC policies, like endowment, money back, limited pay, single premium, and whole life, have different surrender value calculations. This is because of the varying premium structures, investment components, and risk coverage of each policy type.

Step by Step guide to Calculate Surrender Value

So, how do you actually calculate the surrender value of your LIC policy? Here’s a simple step-by-step guide:

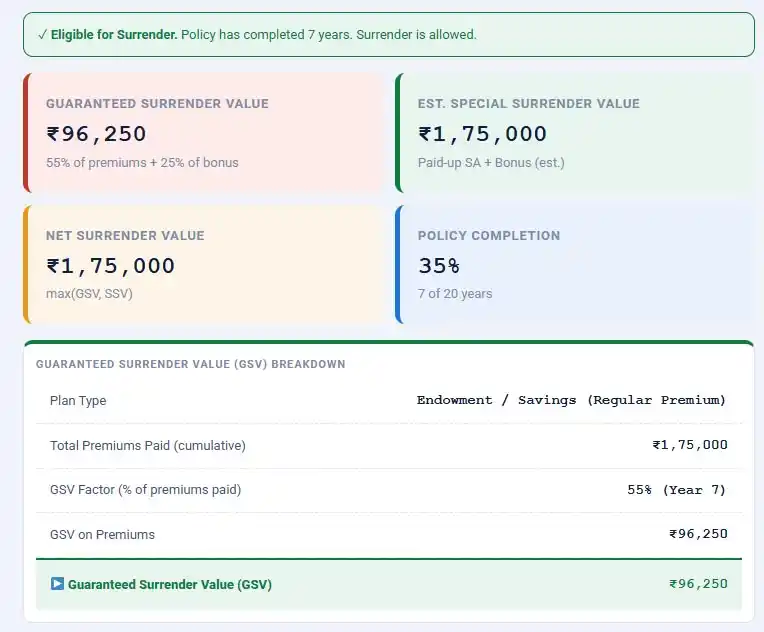

Step 1: Choose your plan type from the options provided (like Endowment / Savings, Money Back, Limited Pay, Single Premium).

Step 2: Enter the sum assured (basic sum assured) for your policy.

Step 3: Input the annual premium (excluding GST) you pay for your policy.

Step 4: Select your policy term in years. For endowment plans, surrender requires a minimum of 3 completed years of premium payment.

Step 5: Enter the number of completed years in force, i.e., the number of full policy years completed as of today. Partial years don’t count.

Step 6: If applicable, provide details of any bonus, optional benefits, vested simple reversionary bonus (if shown on your LIC portal), and outstanding policy loan with interest.

Step 7: Click “Calculate Surrender Value” to see your estimated surrender value.

Let’s take an example. Say you have an endowment policy with a sum assured of ₹5,00,000, an annual premium of ₹25,000 (excluding GST), and a policy term of 20 years. You’ve completed 7 years in force. Using our LIC Surrender Value Calculator and providing the relevant details, you’ll find your estimated surrender value displayed based on these inputs.

Keep in mind that the surrender value calculated by our tool is an estimate based on standard LIC GSV factor tables applicable to most traditional plans. Always double-check your policy’s surrender value with your specific plan’s published premium GSV table before surrendering.

When to Surrender Your LIC Policy

While surrendering your LIC policy can give you a lump sum of money, it’s not always the best move. Here are a few situations when surrendering might make sense:

- Financial emergencies: If you’re facing unexpected expenses and need immediate funds, surrendering your policy can provide much-needed liquidity. But, it’s crucial to weigh the long-term consequences against the short-term gain.

- Better investment opportunities: If you’ve found an investment option that offers better returns than your LIC policy, you might consider surrendering and reinvesting the funds. However, remember that life insurance serves a different purpose than pure investment, so make sure you have adequate risk coverage before making the switch.

- Change in life goals or insurance needs: As you go through life, your financial goals and insurance requirements may change. If your LIC policy no longer fits your needs, surrendering it might be a viable option.

Before deciding to surrender, always calculate the surrender value using our LIC Surrender Value Calculator and compare it with the long-term benefits of continuing the policy. In many cases, staying the course and allowing your policy to mature can provide significant financial advantages.

Maximizing Your LIC Policy’s Surrender Value

If you’ve decided that surrendering your LIC policy is the right move, here are a few ways to maximize your surrender value:

- Pay premiums regularly and on time: Lapsed or delayed premium payments can negatively impact your surrender value. Make sure you stay on top of your premium schedule to maintain a higher surrender value.

- Consider surrendering closer to the policy’s maturity date: The longer you hold your policy, the higher the surrender value. If your financial situation allows, consider surrendering closer to the maturity date to receive a larger payout.

- Explore alternatives to surrendering: Before surrendering your policy, investigate other options such as taking a loan against the policy or opting for reduced paid-up insurance. These alternatives can provide financial relief while allowing you to maintain your life insurance coverage.

It’s also important to understand the tax implications of surrendering your LIC policy. As per current tax laws, the surrender value is tax-free only if the premiums paid are less than 20% of the sum assured. If the premiums exceed this threshold, the surrender value will be subject to taxation as per your income tax slab.

LIC Policies with High Surrender Value

Some LIC policies are known for their high surrender value, making them attractive options for investors looking to balance life insurance with potential returns. Here are a few top contenders:

- LIC Jeevan Anand Policy: This endowment policy combines life insurance with savings, offering a high surrender value. You can use our LIC Jeevan Anand Surrender Value Calculator to estimate your returns based on your policy specifics.

- LIC Jeevan Labh Policy: Another endowment plan, Jeevan Labh, provides a guaranteed surrender value after the policy has been in force for 3 years. To check your potential surrender value, simply input your details into the LIC Jeevan Labh Surrender Value Calculator.

- LIC New Endowment Plan: This policy offers a combination of risk cover and savings, with a surrender value that increases over time. The longer you hold the policy, the higher the surrender value will be.

When considering these policies, it’s essential to look beyond just the surrender value and evaluate the overall benefits, terms, and conditions. Use our LIC Surrender Value Calculator to compare the surrender values of different policies and make an informed decision based on your unique financial goals and circumstances.

Conclusion & My Point of View

By using our LIC Surrender Value Calculator, you can easily check your policy’s surrender value and determine your best options. Wheather you will surrender or not. Remember to consider factors such as your financial goals, policy tenure, and alternative solutions before making the decision to surrender.

If you’re unsure and don’t understand about value of the calculation, don’t hesitate to consult with a financial advisor or LIC representative. They can provide personalized guidance based on your specific situation and help you make the most of your life insurance investment.

Ready to calculate LIC policy Surrender Vlaue? Use our LIC Surrender Value Calculator today and get value of your investment and make an informed decision about your financial future.

FAQs

What is the minimum period after which I can surrender my LIC policy?

Most LIC policies have a lock-in period of 3 years, after which you can surrender your policy. However, it’s essential to check your specific policy document for the exact surrender terms and conditions.

Is there a surrender charge for LIC policies?

Yes, LIC typically deducts a surrender charge from the fund value when you surrender your policy. The charge depends on the policy type and the number of years completed. Surrender charges are higher in the initial policy years and gradually decrease over time.

How is the guaranteed surrender value calculated for LIC policies?

The guaranteed surrender value is a percentage of the total premiums paid, excluding the first-year premium and any extra premiums. This percentage varies based on the policy year and is specified in the policy document. The guaranteed surrender value ensures a minimum payout, even if the fund value is lower.

Can I surrender my LIC policy online?

Yes, you can surrender your LIC policy online through the LIC customer portal. You’ll need to log in, navigate to the surrender request section, and follow the prompts to submit your request. You may be required to upload certain documents, such as a signed discharge form and a copy of your bank passbook or cancelled cheque.

How long does it take to receive the surrender value after applying?

After submitting your surrender request, it usually takes 15-20 days for LIC to process the request and credit the surrender value to your registered bank account. However, this timeline may vary depending on the completeness of your documentation and the efficiency of your local LIC branch.